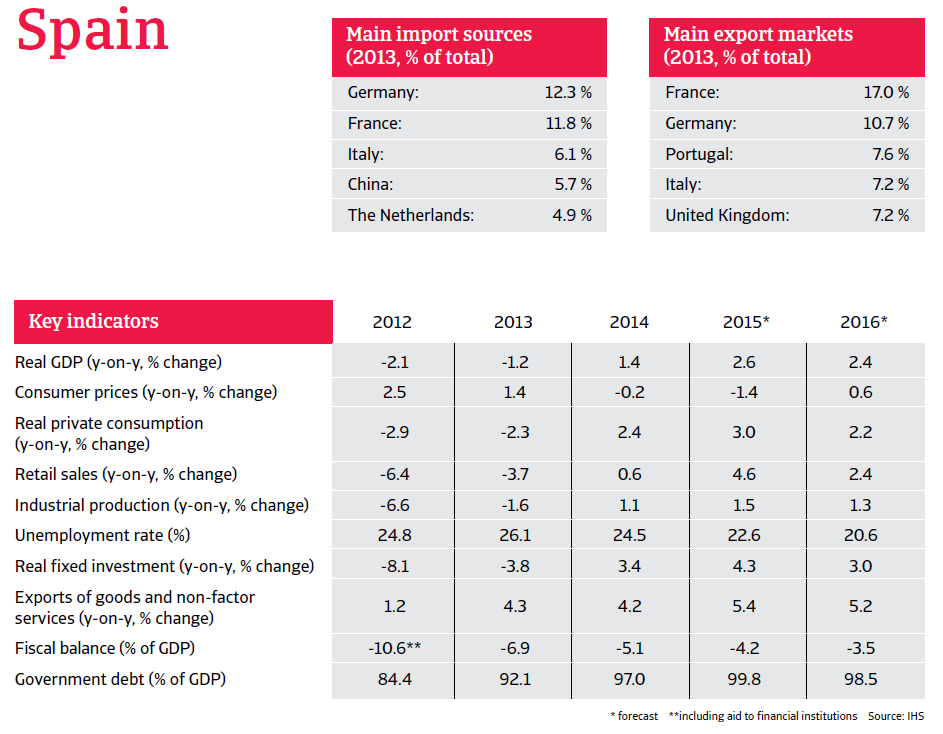

Spain’s real fixed investment and industrial production are expected to continue to grow and exports are also expected to accelerate in 2015.

The insolvency environment

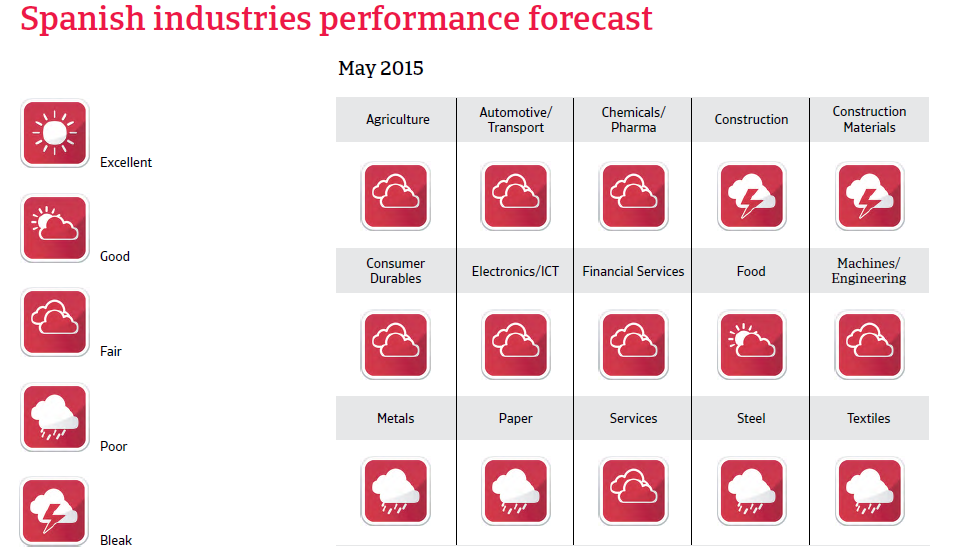

Another insolvency improvement expected in 2015, but figures remain high

Since 2008, corporate defaults have closely reflected economic conditions, with high year-on-year increases in 2008 and 2009. After an annual decrease in 2010 insolvencies increased again in 2011 (15.4%), 2012 (28.4%) and 2013 (16.3%), due mainly to the drop in internal demand and generally high pressure on businesses’ liquidity because of their limited options for external financing.

However, with the economic rebound in 2014 insolvencies started to fall again, by 31.9%. Major decreases were experienced in construction (down 44%), wood/furniture (down 52%) and electronic household appliances (down 46%) recording major decreases. However, business failures in the services sector decreased just 20%, and still accounted for nearly 25% of all business insolvencies.

While another high year-on-year decrease is expected in 2015, this would still leave business insolvencies at a high level of more than 5,000 cases, not yet fully recovered from the increases since 2008, when about 3,000 cases were recorded.

Economic situation

The economic recovery gains momentum

After three years of contraction, Spain’s economic rebound gained momentum in the course of 2014. The rebound was initially due to high net exports, but domestic demand has also recovered somewhat from the severe impact of the rebalancing efforts in response to the construction bubble. Increasing foreign demand and higher business confidence have boosted business investment while a recovering labour market, rising confidence, and pent-up demand for consumer durables have boosted private consumption. Both real fixed investment and industrial production are expected to continue to grow and export growth to accelerate in 2015. Spain’s international competitiveness is improving and its export sector is relatively healthy and competitive.

With the rebound in domestic demand, Spain’s economic performance is now more resilient and sustainable. The economic recovery is expected to accelerate in 2015, with a growth rate of 2.6%.

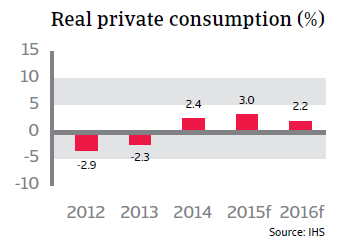

Private consumption remains the backbone of the recovery

Private consumption increased 2.4% in 2014. Private components of domestic demand, essentially consumption and investments, have been the mainstay of GDP growth in 2014 and are expected to remain robust in 2015, with private consumption expected to grow 3.0%. Households’ expectations of their own financial situation benefit from less economic uncertainty and are supported by increased bank lending to consumers, which increased 11.9% year-on-year in 2014.

Deflation woes?

Spanish consumer prices decreased 0.2% in 2014, and are expected to decline further in 2015. This is worrying because, as prices fall, it becomes harder for Spanish debtors to service their debts fixed in nominal terms. Another issue is that deflation tends to suppress demand, as consumers have an incentive to delay purchases and consumption until prices fall further, which in turn could adversely affect economic activity. However, the European Central Bank (ECB) has already taken robust measures to avoid a vicious circle of deflation in the eurozone. Consumer prices are expected to increase again in 2016.

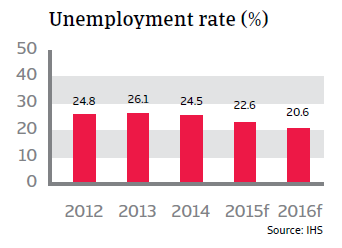

Unemployment decreases, but remains high

Labour market conditions have improved, with unemployment falling from 26.1% in 2013 to 24.4% in 2014. At the same time the decrease in the labour force has also subsided, indicating a further improvement in the labour market. These developments are also a result of labour reforms in 2012 which gave companies more flexibility to set their own wages and working conditions. Unemployment is forecast to fall further in 2015, to below 23%. However, some serious problems remain. 15% of the labour force has been unemployed for more than a year and youth unemployment remains high, at more than 50%.

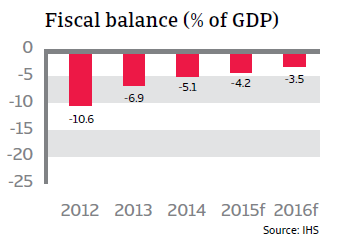

Decreasing budget deficits in the coming years

In 2013 Spain’s fiscal deficit amounted to 6.9% of GDP, while public debt increased to 92% of GDP. Fiscal consolidation to get public spending under control has continued in 2014. Fiscal reforms have been employed to enhance the sustainability of the pension system and to establish a fiscal council. Public debt is expected to peak at 100% of GDP in 2015 while the fiscal deficit is forecast to continue to decrease in the coming years. In 2015 a fiscal deficit of 4.2% is predicted, followed by a reduction to 3.5% of GDP in 2016.